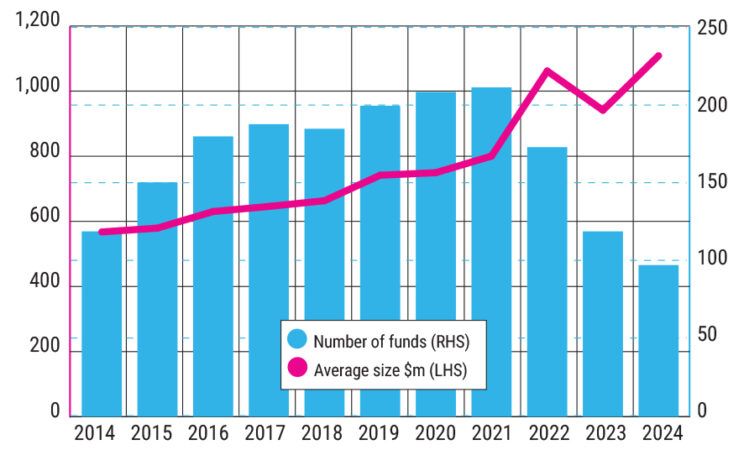

Infrastructure investors have grown comfortable with the idea that ‘bigger is safer’, so much so that the average dedicated infrastructure fund has doubled in size over the past decade, reaching more than $1.1bn in 2024. Despite a smaller number of total funds being raised due to a challenging period for capital raising across private markets amid a broader squeeze on liquidity, the size of the biggest funds has continued to grow.

Average infrastructure fund sizes rising

This trend of increasing scale in the infrastructure market means that these larger funds must double-down on bigger deals to adequately deploy investor capital, leaving behind a significant mid-market opportunity.

The most compelling mix of risk-adjusted return and diversification opportunities, especially in energy transition infrastructure, lies away from the market’s polar extremes – the super-scale end dominated by mega-funds and the venture fringe crowded with start-ups – and instead sits squarely in what some have termed the ‘missing middle’.

Mega-funds funnel ever larger capital pools into low-risk, already scaled infrastructure assets, while venture funds concentrate on start-up climate technology companies. Between these poles sits a widening gap of proven, mid-scale platforms that don’t have the higher risks associated with developing new technologies, but which lack growth capital to realise their broader expansion potential.

Capital advantage: Moving up the value chain

Market conditions increasingly favour capital providers positioned to address this mid-market gap – a theme Schroders Greencoat has been leaning into for some time. Today, there are opportunities to move further up the value chain and invest in assets, projects and companies that are developing in earlier-stage markets, particularly those in their development and construction phases, as ‘platform’ investments to scale up.

These opportunities range from renewable energy developers ready to expand from domestic to regional or global footprints, to developers of adjacent energy transition technologies – battery storage, green hydrogen, district heating – that can accelerate roll-outs once properly capitalised. These opportunities sit comfortably above the technology-risk frontier due to proven concepts, advanced pipelines and clear line-of-sight to offtake, but remain starved of scale finance.

Investment ‘success’ is achieved through providing capital for both organic build-out of new assets, as well as tactical bolt-on purchases of operating assets. This leaves a broad range of exit opportunities ranging from sales to larger infrastructure funds when these platforms have reached a viable scale, to strategic purchases by national, regional or global energy companies, or public listing.

Platform expertise and diversified growth

Platform investing is far more than just buying a single project. It means backing a business that already delivers baseline cash flow through operational assets and with a proven track record, in single or multiple markets, of development, construction and operations.

A recent example is our platform acquisition of an Italian developer and operator of renewable energy, which is active in Italy, France and Spain and has a 1.4 gigawatt pipeline. Our initial €50m investment of growth capital will support in the delivery of further solar and wind projects.

This strategy hinges on portfolio diversification across jurisdictions and technologies to mitigate development or geographic risks and requires investors to align capital strength with sector know-how, often partnering with technology or geography-specific specialists. Operating in the ‘missing middle’, therefore, calls for a blend of capital and expertise through an energy transition infrastructure specialist.

Looking ahead in volatile times

Despite macroeconomic volatility and geopolitical uncertainty, energy transition infrastructure remains resilient. The sector’s inflation-linked cash flows and diversification benefits – via exposure to energy prices and government-backed projects – reinforce its appeal during turbulent markets.

Structural drivers including energy security, amplified by the ongoing conflict in Ukraine, governments’ climate targets, technological advancements in storage, grid modernisation, and AI-driven energy demand are accelerating the need for growth capital in this segment.

This creates a critical opportunity. The ‘missing middle’ offers a dual advantage: exposure to stable, scalable cash flows from operational assets, and participation in high-growth opportunities like renewable expansion, green hydrogen and other adjacent energy transition technologies. The current buyer’s market – characterised by higher interest rates and reduced dry powder – has widened the capital supply demand gap, creating attractive entry points for disciplined strategies.

The boom in mega-funds has pushed infrastructure’s centre of gravity toward fully de-risked, multi-gigawatt assets, portfolios or platforms, yet the most fertile ground now lies one rung below. Despite this era of uncertainty, proven developers still need growth capital to build the next wave of energy-transition platforms, and this intermediate space, ‘the missing middle’, is where value creation meets impact – a fertile ground for investors ready to move beyond the crowded extremes.