In March, the European Commission put forward a proposal to require asset managers to disclose information on the sustainability of their products and portfolios as part of efforts to implement the international climate change agreement signed in Paris in 2015.

Florian Sommer, head of sustainability research at German asset manager Union Investment, (pictured) was part of the group that advised the commission. The proposals included a plan to develop a European taxonomy on what constitutes sustainable investment. “In Germany nuclear energy is being phased out because it’s viewed as dangerous while in France it is viewed as green,” Sommer explained to ESG Clarity‘s sister site, Expert Investor. “It will be very useful.”

Assuming the European Commission plans are implemented they should add further momentum to the sustainable investment push that is taking place across the fund management industry. More than 2000 institutions have now signed up to the UN’s Principles for Responsible Investment (PRI) initiative which provides a framework for implementing ESG integration techniques into a range of investment processes.

“The PRIs are forcing asset managers to think more about ESG integration and active ownership,” Sommer said. “But there is still a lot of room to grow.

Ambiguity remains about how to define and verify environmental, social and governance (ESG) criteria. The UN recently placed about 10 per cent of PRI signatories a watchlist for not demonstrating a minimum standard of responsible investment activity and not taking their commitment seriously enough.

Long-term outperformance

Various studies have looked at the link between sustainability and financial performance. The broad conclusion is that, at the very least, ESG does not underperform conventional investments.

Some studies even claim sustainable investing can outperform because it encourages investors to think outside the box. “Over the long-term it can actually help you to make better investment decisions because it provides the opportunity to invest in companies and technologies which are futureproof,” Sommer continued.

Technological and regulatory shifts over the next few years could radically disrupt a raft of sectors. Governments are clamping down on the use of plastics. Taxes on sugar are being introduced. The fossil fuel industry is grappling with the rise of cheaper and cleaner alternatives. As a result, scores of companies stand to be affected. The coming decades could see the phasing out of everything from the incandescent light bulb to the combustion engine.

“A lot of business strategies may not be around in the future because they are not sustainable,” Sommer says. “Investors need to be aware and understand those risks.

“Sustainable investment funds are not about short-term performance. It’s about working out trends in the future and focusing on companies that are able to adapt.”

The rise in the number of people with Type 2 Diabetes, for example, should benefit Danish pharmaceutical company Novo Nordisk which makes diabetes treatments.

On the other hand, companies such as Coca-Cola and PepsiCo that make the bulk of their revenues from sugary soft drinks could face significant challenges.

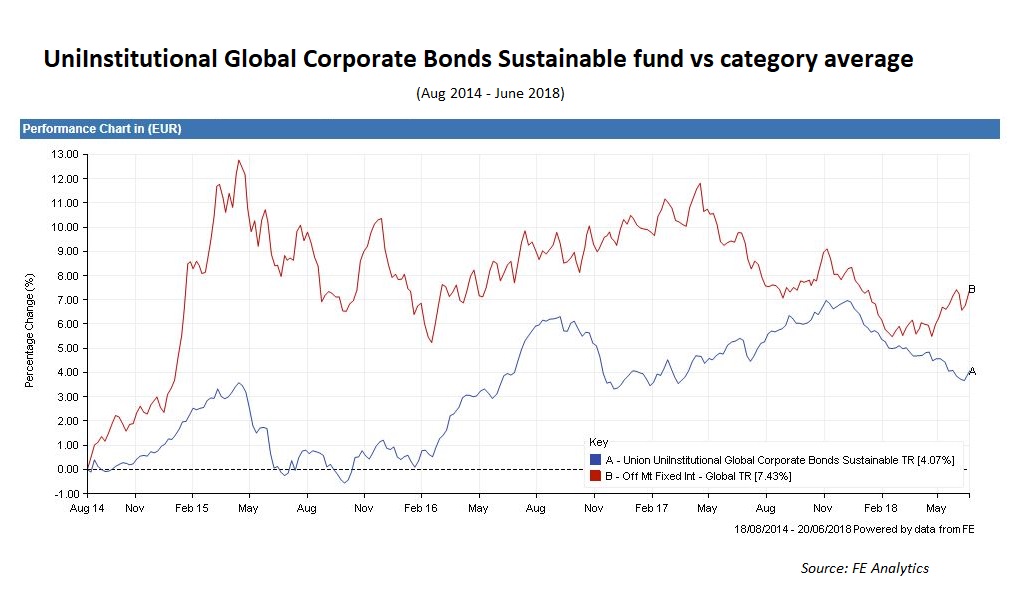

Investors in Union Investment’s UniInstitutional Global Corporate Bonds Sustainable fund may be banking on longer-term results. Since it launched in August 2014, the fund has posted returns of 4.06 per cent compared to the category average of 7.43 per cent, according to FE Analytics.

A broad church

Union Investments has more than a hundred socially responsible funds including institutional mandates – covering everything from global equities to green bonds to meeting the UN Sustainable Development Goals – and it manages €34bn dedicated to sustainable assets.

The group has developed its own software platform, into which it inputs ESG data from various providers to generate sustainability ratings for more than 8000 companies.

The group’s investor clients vary from large institutions to private clients.

“Sustainability is a broad church and there are a lot of issues beyond environmental and social issues,” Sommer continued.

“A church bank, for example, has very different views about sustainability than an insurance company or a corporate pension fund. They are different institutions.

“We do not tell individual clients how to do sustainable investment. What we do it talk to them and find out what their values and ethical boundaries. It’s a customised approach.”

Emerging markets

ESG may have become a principal concern in the European asset management industry over the last couple of years but emerging markets now account for the majority of global growth. In many developing countries, socially responsible investing is barely on the radar.

On the day we meet, Sommer is scheduled to fly to China. The Beijing government avoided the country’s environmental issues for years. But in the face of chronic air pollution and widespread habitat destruction President Xi Jinping has made the environment a priority.

“It’s a massive challenge but China is transitioning,” Sommer says. There is tremendous growth in green solutions.”

China is now the world’s largest market for both photovoltaics and solar thermal energy and its electric car market is growing twice as fast as the US.

“The most interesting place to watch at the moment [as a socially-responsible investor] is China because no other country has the same level of environmental targets and ambitions and it has the political system to force it through.”

This article originally appeared on ESG Clarity‘s sister site, Expert Investor.