The investment landscape “looks as uncertain as it has for some time”, with growth, inflation, monetary and fiscal policy, politics and geopolitics all potential drivers of volatility. However, in many countries across the globe, fiscal policy and regulatory support for sustainability are progressing, with corporate disclosure, fund labelling and green bond standards – among many other incentives – coming into place.

Fixed-income fund managers, therefore, are predicting the market will continue to grow throughout 2025, with evolution expected as it rolls up its growth curve.

Despite this, some investors are observing the continued tight level of credit spreads and choosing to stay on the sidelines – a move that risks missing out on what could be another solid year for credit investors, according to Damien Hill, senior portfolio manager at Insight Investment, who described 2025 as a year of “ample opportunity” for active fixed income managers.

With multiple moving parts to consider, PA Future asked fund managers for their thoughts ahead of a potentially turbulent year.

Takeaways from 2024

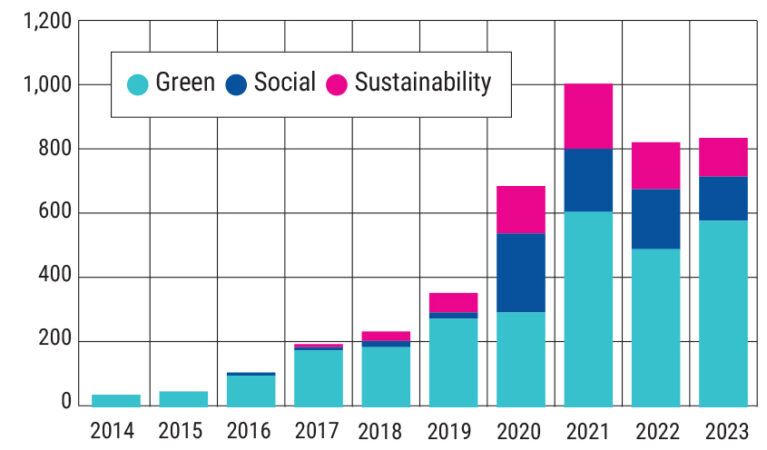

Last year, Stephen Libertore, Nuveen’s head of ESG/impact for global fixed income, predicted a record year for labelled Green, Social and Sustainable (GSS) bond issuance. However, the prediction didn’t quite come to fruition.

“[At the time of writing] We have seen $986bn of issuance, down 1.2% from 2023 and 14.2% lower than 2021’s record of $1.1trn. The slight drop in overall issuance was concentrated primarily in the Sustainability-Linked Bond (SLB) structure, which fell by 55.2% compared to 2023 because of market concerns around credibility and greenwashing,” Libertore explained.

“Three of the four use-of-proceeds (UoP) structures grew over the course of the year, with green bonds remaining the predominant structure at 60.9% of the total, while transition bonds benefitted primarily from Japan’s initiation of its GX Plan +497.1% ti $20.3b.”

According to Libertore, these results are a good reminder of a couple of factors that should always be kept in mind when evaluating this space.

“First, just because something is labelled a green bond doesn’t mean it is, and just because it isn’t labelled a green bond doesn’t mean it is not. Our approach is solely focused on evaluating the underlying UoP to determine if they are in alignment with our proprietary impact framework. As a result, securities that have rapidly grown in the market like debt-for-nature swaps and outcome bonds do not qualify for inclusion because they are not labelled, despite generating material and differentiated impact.

“It also highlights that despite being unique securities that direct proceeds to specific uses, they are still fundamentally bonds and are subject to the myriad of issues that affect fixed-income issuance. Therefore, as with the broader debt market, issuance of labelled securities was impacted by more persistent inflation, uncertainty around global monetary policy and increasing geopolitical risk. Despite the headline miss, granularity and specificity continued to increase the overall opportunity set, which is a distinct positive for us as an active total return manager, and a further indication of the maturation of the market.”

Continued growth trajectory for green bonds

Looking ahead to 2025, signs of improvement for sustainable issuers – and, therefore, sustainably focused products – through 2024 are expected to continue, supporting a continued growth trajectory for green bonds, according to Rob Lambert, portfolio manager at RBC BlueBay Asset Management.

In Europe, rising regulatory and policy support, such as mandatory climate disclosures and carbon reduction targets, is expected to encourage sustainable finance, continued Lambert, with the EU’s Sustainable Finance Action Plan and similar initiatives driving incremental demand for green bonds.

One such initiative happened late in 2024. On 13 December, the European Securities and Markets Authority released Q&As addressing specific aspects of its guidelines on fund names incorporating ESG or sustainability-related terms, with key clarifications relating to funds investing in European green bonds. Notably, these are exempt from certain investment restrictions related to company exclusions, such as for exposure to energy generation with fossil fuels, flagged Pietro Sette, research director at MainStreet Partners.

“Fund managers may apply a look-through approach to assess whether financed activities respect such exclusions, rather than the issuer itself. Once again, this highlights the importance of green bonds in financing the energy transition, especially for key sectors such as utilities and industrials.”

Libertore expects green bonds that fund renewable energy and energy distribution projects to remain the leading source of issuance in the labelled space, as the energy transition, especially at the utility-scale level, “remains unabated”, given the financial advantages seen in a variety of renewable generation type’s levelised cost of energy.

Additionally, given the recent commitment from more than 500 companies to report on biodiversity risks following the Taskforce on Nature-related Financial Disclosures’ recommendations, some of these companies might leverage these disclosures to allocate green bond proceeds to biodiversity projects, according to Michiel de Bruin, portfolio manager and head of global fixed income macro at Robeco.

“Similarly, the recent publication from the Climate Bond Initiative on the Climate Resilience Taxonomy might support further issuance of green bonds that tackle climate adaptation projects. The market has become more mature thanks to the higher diversification among different issuer types. Still, this diversification trend will continue in 2025, especially within the emerging markets space and hard-to-abate industries.”

Expanding social bond issuance

Social bond issuance addressing affordable housing should also continue to expand next year.

“We have seen the topic dominate politics globally as affordability has continued to decline due to more persistent inflation and ongoing skilled labour shortages. In response, we expect that increasing funding will be made available in order to help increase accessibility across sectors and markets,” Libertore added.

This was also noted by Tammie Tang, senior portfolio manager at Columbia Threadneedle: “As a bond investor for positive social outcomes and social impact, we are encouraged by social labelled issuance from the likes of governments, development banks, non-profits, corporates and financials.

“Many factors will affect the ultimate GSS supply for the year ahead, including consideration of regional politics and sector or issuer-specific issues. Nonetheless, we expect GSS or labelled bond issuance to remain a meaningful portion of primary market activity. We continue to consider GSS issuance meaningful and positive in the context of supporting the provision of capital to help address our social and environmental challenges.”

Challenges for SLBs and the blue economy

However, SLBs continuous decline as a percentage of GSS bond issuance “is raising serious questions regarding the survival of the label”, according to Sette.

“Sustainability-linked instruments are caught in the crossfire between growing scrutiny on ESG credentials and increased relevance of green bonds in European sustainable finance regulation, namely the Sustainable Finance Disclosure Regulation and the European Green Bonds Standard,” he said. “Yet there is cause for optimism, and there’s hope for a resurgence in 2025 as key emission targets align with bond tenors.”

Kris Atkinson, lead portfolio manager at Fidelity International, also spoke of his concerns about funding for the blue economy: “Funding remains a key issue with UN Sustainable Development Goal (SDG) 14: Life Below Water – the least funded of all 17 UN SDGs. Institutional capital has been slow to flow into the sector, partly because the blue economy is still viewed as a thematic investment approach, requiring investors to recognise its coherence as a market.

“So how can bond investors help address the funding issue in 2025 and beyond? Well firstly, we need to leverage existing industries. While much attention is given to early-stage start-ups, significant opportunities exist within the $3trn ocean economy.

“Focusing on transitioning established businesses to more sustainable practices could drive immediate and scalable impact. Furthermore, we need to continue the momentum of financial innovation in the blue finance space. Specific to fixed income, innovative instruments like blue bonds and debt-for-nature swaps are gaining traction but remain nascent as markets.

“This is not philanthropy; this is a transformative investment opportunity.”

Watch out for regulatory and trade policy change

Meanwhile, Rathbone Greenbank fund manager, Stuart Chilvers, highlighted the meaningful dispersion developing in interest rate expectations in Europe compared to the US and the UK, driven by weaker growth and concerns over the potential implications of US trade policy on growth.

“Given the high level of uncertainty on US trade and fiscal policy and ongoing political uncertainty in Europe, it will be crucial in 2025 to be nimble in our duration exposure to various markets as we get greater clarity on policy and their likely implications for interest rates.”

Any change or progress in the regulatory space in the US or Europe has the potential to affect the industry, added de Bruin: “Early adopters of the EU Green Bond Standard could give some guidance on the appetite for investors for these instruments, which could have a pass-through effect on the ‘greenium’ and provide more incentives to green bond issuers. In the US, any modifications to the Inflation Reduction Act or further pushback against ESG could lead green bond issuers to step away or change the priorities of their allocation of proceeds.”