The number of sustainable funds considered in Morningstar’s universe grew by 51% in the third quarter, as a result of more groups moving to classify funds under the Sustainable Finance Disclosure Regulation (SFDR).

Meanwhile, sustainable fund flows and assets considered to outpace the wider universe leading to global sustainable fund assets to almost double over the past six months to top $3.9trn.

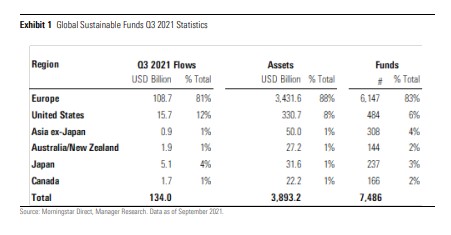

The latest Global Sustainable Fund Flows for the third quarter of 2021 shows global sustainable funds attracted $134bn in net inflows for the three-month period – this was a decline of 15% compared to the previous quarter but higher than a year ago, and shows sustainable funds are in favour compared to non-sustainable funds where inflows fell 20% in Q3.

Overall, there were 270 sustainable fund launches around the world – 63% of these took place in Europe but the US saw a record number of new funds with 38 products coming to market.

SFDR

The number of funds now considered sustainable in the Morningstar’s global universe has grown by 51%, which the ratings firm said is down to the introduction of SFDR on 10 March.

“SFDR requires asset managers to provide detailed ESG information on their strategies,” the report said. “As a result, the volume and quality of ESG-related disclosures in legal documents have substantially increased. New ESG language meeting our criteria to classify a strategy as sustainable has led to an increase in the number of funds included in our universe, which at the end of September was composed of 6,147 sustainable products, up from the 3,730 funds we originally reported at the end of June. This represents a 65% growth.”

It also noted Morningstar is likely to report a larger sustainable fund universe going forward as the data team continues to review ESG language that aligns funds with SFDR as there is “a high level of overlap between our eligibility criteria and those for Articles 8 and 9 of SDFR”.

The report also highlighted the number of “repurposed” funds that have updated legal documents to meet SFDR requirements has dramatically increased – the data team has so far this year identified as many as 3,111 additional products with qualifying language.

“Asset managers seized the opportunity of publishing new SFDR-compliant prospectuses to enhance their funds’ ESG integration strategies, add exclusions, switch funds to ESG-focused mandates, and, in some cases, rebrand existing strategies,” the report said.

Europe

Sustainable fund flows in Europe represented nearly half of overall fund flows albeit this is lower than previous quarters. Flows were recorded at $10.8.7bn, 17.6% less than the $131.9bn stated in Q2, and a larger dip then the 15.5% in inflows in conventional funds.

Morningstar said this was down to fixed income funds being popular with investors but there being far fewer options in the sustainable bond fund space.

BlackRock, Amundi and Swisscanto saw the lion’s share of flows for Q3, while Fidelity, Janus Henderson and Storebrand saw the highest outflows.

US

The US sustainable fund landscape saw $15.7bn in net inflows, a 12% drop on the previous quarter and the lowest quarterly amount this year. However, broader US market funds registered a steeper decline of 29%.

Passives continued to dominate with 61% of sustainable fund flows, but this is to a smaller degree than in the past – passive sales reached a record 83% in Q1 2020.

The report also noted 61% of flows into sustainable fixed-income funds have been growing steadily, crossing the $2bn threshold for the first time in the third quarter of 2020 and staying above that marker since.

Asia ex-Japan

Outside of China, Asia ex-Japan’s third quarter net inflows surpassed the second quarter by 43%, Morningstar said. This was driven by a strong net flow of $1.9bn from Taiwan into a single fund – the newly launched of Shin Kong Environmental Sustainability Bond Fund, which raised about $945m.

Assets in Asia (excluding China which did not have available data at the time of writing for the report) grew by 7% in Q3 to reach $14.3bn with Taiwan overtaking South Korea as the second-largest sustainable fund market.

Moodys: Green and sustainability-linked bond issuance to top $1trn in 2021

Meanwhile, Moody’s has predicted issuance of green, social, sustainability and sustainability-linked (GSSS) bonds is set to exceed $1trn by the end of this year, up 64% from $614bn last year

Moody’s ESG Solutions predicted momentum for GSSS bonds seen in the last quarter of 2021 will continue, underpinned by an increased market focus on accelerating climate action and realizing sustainable development objectives.

In the first three quarters of this year, global issuance of GSSS bonds came to $775bn, nearly double the $402bn issues in the first nine months of 2020.

The third quarter of this year saw GSSS issuance of $217bn – 21% lower than the second quarter of 2021 – of which were $115bn were green bonds, $29bn social bonds, $52bn sustainability bonds and $21bn were sustainability-linked bonds.

Green bond issuance for the first three quarters of this year, at $380bn, was up 75% compared to the same period in 2020.

Moodys expects 2021’s GSSS issuance to include over $500bn of green bonds, $200bn each of social bonds and sustainability bonds and $100bn of sustainability-linked bonds.

One of the trends behind the significant rise in GSSS issuance this year, according to Moodys, is the coronavirus crisis putting social financing to the forefront of sustainable debt markets. The group said this trend is likely to continue well after the recovery from the pandemic.

Another notable source of momentum, Moodys said, was COP26, which could provide a framework for global cooperation on carbon pricing, increase climate finance for developing economies and spur the mobilisation of capital for investing in climate resilience.