A limited choice of easily identifiable labelled products for investors to choose from, and the absence of passive products, are the main concerns as the deadline for managers of UK sustainable funds to comply with the Sustainability Disclosure Requirements (SDR) passed last week (2 April).

That’s according to the latest report published by Morningstar Sustainalytics – UK SDR Labeled and Nonlabeled Fund Landscape – which examines the characteristics of the funds in each universe, the metrics used to report on sustainability and the most popular companies held by labelled funds.

Also read: FCA delays SDR implementation for portfolio managers

Although SDR appears to be achieving the objective of matching sustainability claims with objectives, the report concluded there continues to be a significant degree of “wait and see”, with the slower-than-expected adoption of labels contributing to the FCA shelving plans to publish an extension of SDR rules to portfolio management services.

Further, a PA Future Freedom of Information request has revealed that between 29 November 2023 and 18 March 2025, the FCA was made aware of four firms having disengaged with the process of filing for a label after initially filing amended disclosure applications for at least one of their funds – although firms may subsequently decide to change their mind and re-apply.

“The 2 April deadline for the SDR naming and marketing rules has passed, and the picture of the UK labelled and non-labelled fund landscape has yet to be complete.” said Hortense Bioy (pictured), head of sustainable investing research at Morningstar Sustainalytics.

“It’s been a long process, but the result should help sustainability-conscious investors better understand what they are investing in. As the landscape of UK funds with sustainability characteristics continues to evolve in the coming months, investors will need to understand how SDR has affected their portfolios.”

Key findings

The Morningstar Sustainalytics report, which examined how the sustainability disclosure requirements have reshaped the UK ESG fund market, found by the end of March, 80 UK open- and closed-end funds had opted for one of the four SDR labels, representing £34.5bn in assets under management and accounting for 20% of the overall universe of funds that claim sustainability characteristics. To put that in perspective, at the end of 2023, the FCA predicted that as much as 45% of the 630 UK funds with key sustainability-related terms in their names or objectives could use a label.

Focus is the dominant label, representing 56% of all labelled funds, followed by Impact (26%), Improvers (13%), and Mixed Goals (5%). Schroders provides the most labelled funds, followed by Liontrust, M&G and Columbia Threadneedle.

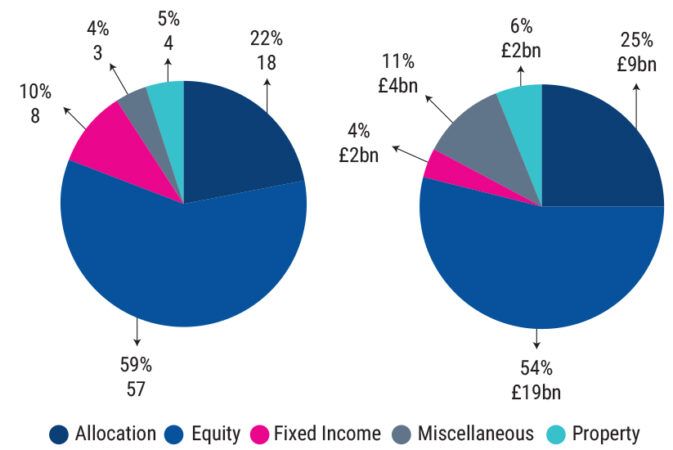

All labelled funds are actively managed. Global large-cap equity strategies dominate, while fixed-income funds are underrepresented (31% and 4% of total assets, respectively).

Breakdown of labelled funds by broad asset class (number of funds and assets under management)

Of note, the majority of allocation funds have opted for the Focus label, rather than Mixed Goals. The use of a single label for multi-asset funds can be explained by the adoption of a single sustainability approach for both equity and bonds, the report said, but this may make it challenging for investors looking to build diversified sustainable portfolios.

Non-labelled universe

As of the writing of Morningstar Sustainalytics’ report, 325 UK-domiciled funds were classified as non-labelled funds, representing £280bn in assets. Therefore, the non-labelled fund universe is almost four times larger than the labelled funds in terms of the number of funds, and eight times larger in terms of assets under management.

It is unknown, however, how many funds may be close to meeting label requirements but elect not to be constrained by measuring and meeting the associated criteria on a perpetual basis.

To comply with the SDR naming and marketing rules, many funds were forced to change their names, dropping sustainability-related terms or swapping with others. Among the funds that dropped terms, several belong to the Stewart Investors range. For example, Stewart Investors Asia Pacific Leaders Sustainability became Stewart Investors Asia Pacific Leaders.

“One of the requirements of the SDR regime is that investment managers develop and apply a specific and measurable sustainable objective and related key performance indicators to all portfolio companies. We believe companies can contribute to sustainable development in different ways and that it is helpful to evidence that contribution using measures and methods that are suitable for each company,” a spokesperson told PA Future.

“We remain committed to investing transparently in high-quality companies with strong management teams that are well placed to contribute to, and benefit from, sustainable development, and this commitment will not change.”