Impact investing is showing signs of maturing, with investors taking increasingly sophisticated approaches when it comes to performance and capital allocation.

This is according to the Global Impact Investing Network (GIIN), in its new report Impact Investing Decision-Making: Insights on Financial Performance, which found impact investors are exercising a multi-dimensional approach to their decision-making to achieve satisfactory financial and impact performance in line with their goals.

The report looks at how five investors – Anthos Fund & Asset Management, IDP Foundation, Incofin Investment Management, UBS Global Wealth Management, UBS Optimus Foundation, and Vox Capital – are considering the following:

- Financial return objectives

- Impact objectives

- Financial risk tolerance

- Impact risk tolerance

- Resource capacity

- Liquidity constraints

“To understand what success looks like, impact investors are looking at how they can most efficiently achieve the best impact and financial performance – the most optimal performance point – for the least amount of capital deployed,” said GIIN director of research Dean Hand.

“Experienced impact investors exercise a multi-dimensional approach to decision-making, considering impact objectives and impact risk alongside traditional factors.”

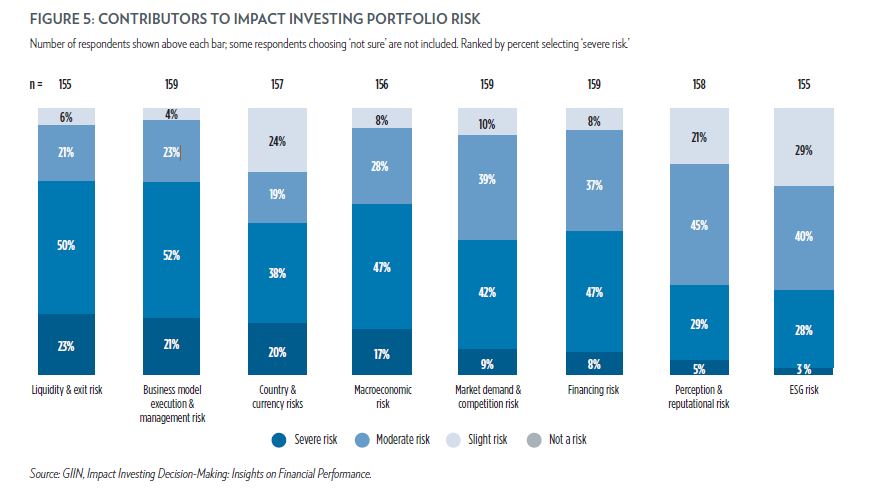

When it comes to risk, the report found the largest share of investors reported perceiving at least ‘moderate’ business model execution and management risk, and liquidity and exit risk (73% of investors for both). More than half of investors also perceived moderate or severe country and currency risk, financing risks, and market demand and competition risk.

“Perception of financial risk also varies by peer group”, the report said. “The share of private equity-focused investors perceiving severe liquidity and exit risk is four times greater than the share of private debt-focused investors (28% versus 7%)”.

“By contrast, a greater share of private debt-focused investors perceives severe country and currency risks (29% versus 19% of private equity-focused investors and 12% of real assets-focused investors). Further, 36% of emerging market-focused investors perceive severe country and currency risks, compared to just 4% of developed market-focused investors.”

Private debt

The report also looked at the financial performance of areas more broadly.

In private debt it found impact funds generate stable financial returns on a risk-adjusted basis. On the GIIN’s 2020 Impact Investor Survey, gross realized, average financial returns ranged from 8% for developed market investments to 11% for emerging market investments.

Financial returns across private debt investments tend to align with investor expectations. More than a quarter of private debt-focused investors (26%) reported outperforming their financial expectations and 24% reported outperforming their impact expectations; these same figures stood at 16% and 18%, respectively, for private equity-focused investors.

It also found impact debt funds can play an important role in risk reduction and diversification, saying ‘on a risk-adjusted basis, the private debt impact funds in the Symbiotics research have demonstrated strong financial performance, with the highest Sharpe ratio (5.17) across asset classes assessed in the study’.

Private equity

GIIN’s perspective on private equity is that private equity impact investments can generate market-rate returns, depending on varying investment goals and objectives.

It also said financial returns vary significantly, with widespread dispersion in financial performance. ‘As in mainstream financial markets, impact investments demonstrate significant variation in returns, with an average standard deviation of 9.68%, based on the Cambridge benchmark’.

Lastly, the report found investors’ objectives shape financial performance; and smaller funds tend to outperform market and investor expectations.

Real assets

Real asset impact investors can generate market-rate returns, but realised returns vary widely, the report said. “Realised returns vary significantly not only by time horizon and segment but also within segments, reflecting wide dispersion and potential to generate market-rate returns or underperform relative to comparable benchmarks.”