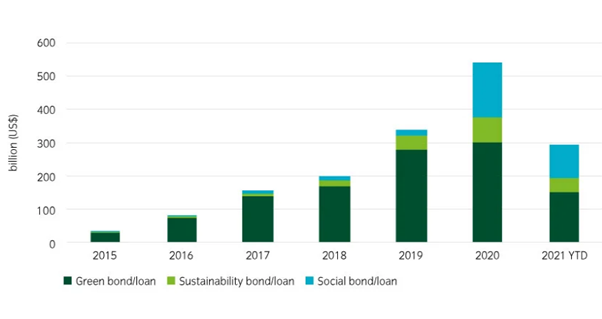

The impact bond market is growing rapidly. After total issuance rose over $1trn last year, it is on track to near $2trn by the end of 2021. Growing demand from investors for a clear positive environmental or social impact with their portfolios, as well as a surge in issuance to support communities and economies through the coronavirus pandemic, have helped drive this growth.

However, a significant challenge remains for investors. A lack of clear standards and oversight make investors susceptible to ‘impact washing’, where an issue might claim to be ‘green’ or ‘social’, but with little measurable positive impact – or no means of determining whether it has achieved its stated goals.

This is now widely recognised, but a widely accepted solution is still to be developed. This is forcing investors and asset managers to conduct their own due diligence to ensure that the impact they seek is being delivered by the assets in which they invest.

The two most common types of impact bonds are green and social bonds. Green bonds dominate the impact bond market, accounting for 53% of issuance in 2020. Notably, in 2020, social bond issuance jumped almost nine-fold to $161bn, up from $18bn in 2019, propelled by the global response to Covid-19.

Proceeds from green bonds are typically used for projects such as renewable energy, pollution prevention, climate change adaptation and sustainable water management; while proceeds from social bonds are used to fund social projects including health, education, sanitation, and socioeconomic empowerment.

Issuance has continued to surge in 2021. We expect to see significant growth in US issuance, as US corporates have been moving to align their financing with their messaging.

Impact bond issuance has grown rapidly

Impact washing

Impact washing is a real concern. Of the 285 impact bonds issuers Insight has analysed since 2017 to the end of 2020 from a sustainable impact perspective, it has been disappointing to see that only 34% have met all our requirements to receive a green rating under our impact bond assessment framework. Conversely, 16% received a red rating meaning they did not pass our minimum sustainability criteria, with the remaining 50% rated amber, indicating there are some weaknesses in their approach.

Our impact bond evaluation process includes three ‘pillars’ assessing the ESG performance of the issuer, the strengths of the bond framework and its use of proceeds and then also a qualitative and quantitative analysis of the positive impact of the bond. Weaknesses identified might include a lack of clarity as to how proceeds will be used, no independent verification of the use of proceeds, or concerns over how the ultimate impact of projects would be measured and reported.

Although there are commonly used frameworks and standards, such as the International Capital Market Association’s Green Bond Principles, or the equivalent Social Bond Principles, these are not a prerequisite for issuance – and only cover a portion of the universe. Other initiatives including the EU taxonomy, part of the EU’s wider Sustainable Finance Action Plan, may help to standardise issuance criteria.

However, significant progress is yet to be made. Until then, investors will need to identify whether bond proceeds are used as initially marketed or are simply ‘green’ or ‘social’ in name only.

Case study

In 2020 we rated a social bond that had been issued by a prominent financial institution as red under our impact bond assessment framework for failing to meet Insight’s sustainability requirements. The bond lacked several key features:

- Clear reporting guidelines and key performance indicators

- Detailed information on if the proceeds would be used for financing or refinancing

- A strong framework for creating and measuring impact

While an impact bond may remain attractive for our clients and portfolios from a financial perspective, for clients and portfolios with specific sustainability targets or criteria, a red rating may lead us to avoid investing.

Our impact bond assessment framework has helped us focus on sustainable issuance with clear, measurable positive effects, aside from their financial characteristics. As the market grows, we will continue to carefully evaluate new issuances for clients seeking to make an environmental or social impact.

Investing in impact bonds is one way fixed income investors can achieve a positive environmental or social impact. Better client outcomes require appropriate processes to interrogate each bond because labels alone do not guarantee bonds achieve what investors expect.