Analysis of regional benchmarks in the US and Europe has indicated the US is closer to reaching net zero emissions, defying expectations the eurozone has been ahead in terms of carbon reduction.

A report by Qontigo, The Best Bang for You Climate-Aware Buck, looked at STOXX Paris-Aligned benchmarks (PABs), the STOXX Europe 600 index and the STOXX USA 500, and found the US is closer to the ultimate goal of net zero emissions than Europe, in contrast to emissions compared with GDP.

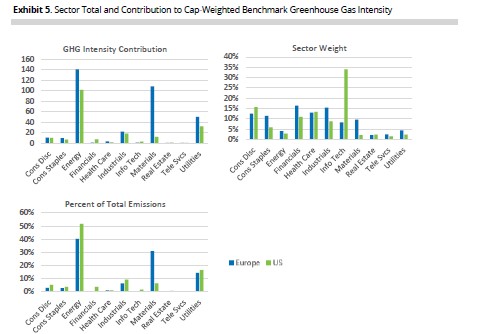

This was largely driven by the US having a higher concentration in less carbon-intensive sectors such as technology, while Europe had higher greenhouse gas (GHG) intensity with companies in the materials sector making up a significant segment of its listings.

The report, authored by Melissa Brown, global head of applied research at Qontigo, said: “Our initial expectation was predicated on the fact that carbon reduction has been a focus of European regulators, companies and investors for quite some time, whereas US-based investors have been concerned about the potential give-up in returns. At the same time US regulators were at best indifferent and at worst actively advocating against such portfolios, unless managers could prove returns would be higher or risk would be lower. Given this, we expected the initial starting point (the underlying capitalisation-weighted benchmark) would already be more climate-friendly in Europe.

Tech accounts for more than one-third of the market value of the STOXX USA 50 and has very low GHG emissions intensity, while materials accounts for more than 30% of the GHG intensity level of the STOXX Europe 600. In the US, the materials sector accounts for less than 10% and, furthermore, energy stocks – which are the biggest contributors to an index’s overall GHG intensity – made up a smaller part of the index in the US.

The report added: “An important point to note is about further reductions in GHG emissions to meet the 7% per year goal. Starting from a much lower base in the US suggests that the goal will become increasingly more difficult to meet.”

However, author of the report Brown was quick to point out these findings could be a little misleading.

See also: – Lack of regional ESG products causing ‘unintended risks’ in managed funds

“[This outcome] reflected the disconnect between the US stock market and its economy. According to OECD, US GDP is actually 70% more carbon intensive than Europe’s. The weights of sectors in the market index are far different from their GDP weights. If we broaden our market definition in the US to the STOXX USA 900 (more of a large-mid cap index than just large cap like the USA 500) and analyse just the 400 stocks in the USA 900 that are not in the USA 500, we get a somewhat different story.”

Brown broadened the research to include mid-cap names in the names, and dilute the effect of the tech mega-caps, and calculated some of the same statistics for the USA 900, as well as for the 400 stocks in the USA 900 that are not in the USA 500.

See also: – Five ways to decarbonise a portfolio: A timeline of techniques

It found the smaller names in the USA 900 had more emissions—roughly equivalent to those in Europe—and the Paris-Aligned benchmark had a smaller overall reduction from them, compared with the larger, more tech-dominated names.

“This was closer to what we would expect, knowing that the US has higher emissions as a percent of GDP than does Europe, but It does not erase the apparent discrepancy,” Brown said.

She also highlighted if energy prices continue to rise and the weight of the energy sector in the US increases, but companies in the sector do not work to reduce emissions, the required 7% reduction in emissions from the prior year will be more difficult to achieve. This is especially true if the increase in energy weight comes at the expense of a decrease in the lower emissions sectors, such as tech.

Brown concluded: “We remain firmly convinced that the Paris-Aligned Benchmark methodology offers companies substantial incentives to reduce emissions and be included in the benchmark. As more and more investors shift their investments into these kinds of strategies, this will be a win-win—not only for the environment, of course, but also for investors who will be able to invest in a well-diversified, broad-market benchmark.”