Intentional ESG offerings can display a broad array of characteristics, making it hard to compare them side by side. But when it comes to dedicated impact funds, one thing they have in common is the aim of bringing a clear sense of purpose to investors.

They can be deemed as funds that look to invest in companies helping to solve the world’s problems, while also providing measurable impact. It is then incumbent on the portfolio manager and analysts to attempt to measure the positive environmental or social outcomes of a given investment, as well as at the portfolio level.

Providing precise results can be tricky but the final outcome is shaped through a mix of a company’s own reporting, external data and analyst assessments. This is usually laid out in an in-depth report produced annually or half yearly, highlighting how, on aggregate, holdings have fared. Impacts that are commonly assessed in such a manner include tonnes of CO2 saved, penetration of renewable energy, healthcare provision, water efficiency and social inclusion.

But as well as providing evidence of impact, one shouldn’t lose sight of investment-orientated factors. We bring all these elements to life by looking at three impact funds: Baillie Gifford Positive Change, M&G Positive Impact and Montanaro Better World.

Diving into three impact funds

All three hold the Low Carbon Designation from Morningstar, reflecting the fact that there is low carbon risk and little to no fossil fuel involvement in the portfolios.

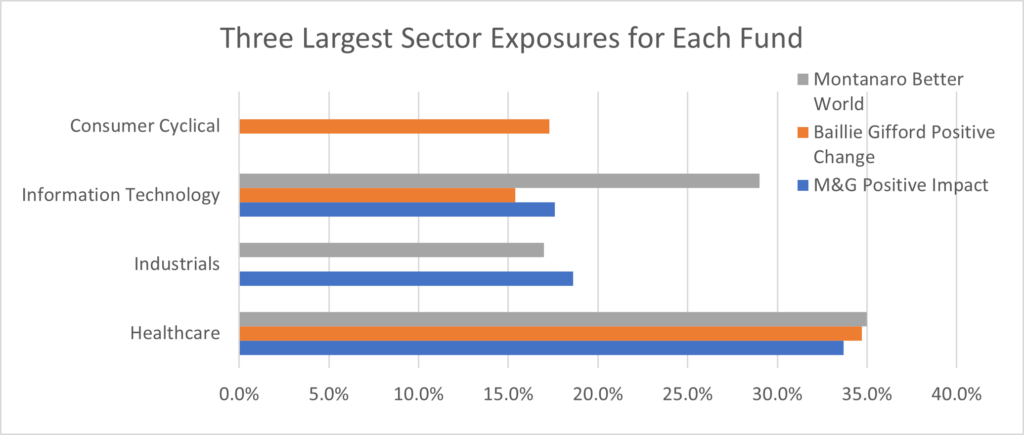

When it comes to sector exposures, healthcare and information technology feature heavily, but it’s healthcare that’s the largest in each case at around a third of the portfolio. This can be a common trait when it comes to impact funds where there is a close eye on medical innovation.

The corollary of this is that in pharmaceutical research and development, animal experiments need to be carried out to determine drug safety and efficacy. Therefore, animal testing for medical purposes does take place. There would rarely be drug discoveries if this wasn’t the case and the chart below using Sustainalytics data is reflective of this dichotomy, showing the portfolios’ percentage exposure to companies involved in animal testing. The table also shows the absolute number of companies held that flag up on this side. The number here is linked to the total number of holdings in the portfolio and the managers’ respective approaches in terms of concentration. Montanaro has 50 holdings in total, while the other two are slightly above 30.

Exposure to animal testing and number of companies involved

| Fund | Product involvement % of portfolio – animal testing | Number of holdings with animal testing |

| Baillie Gifford Positive Change | 29.75 | 11 |

| Montanaro Better World | 29.09 | 15 |

| M&G Positive Impact Sterling | 28.75 | 9 |

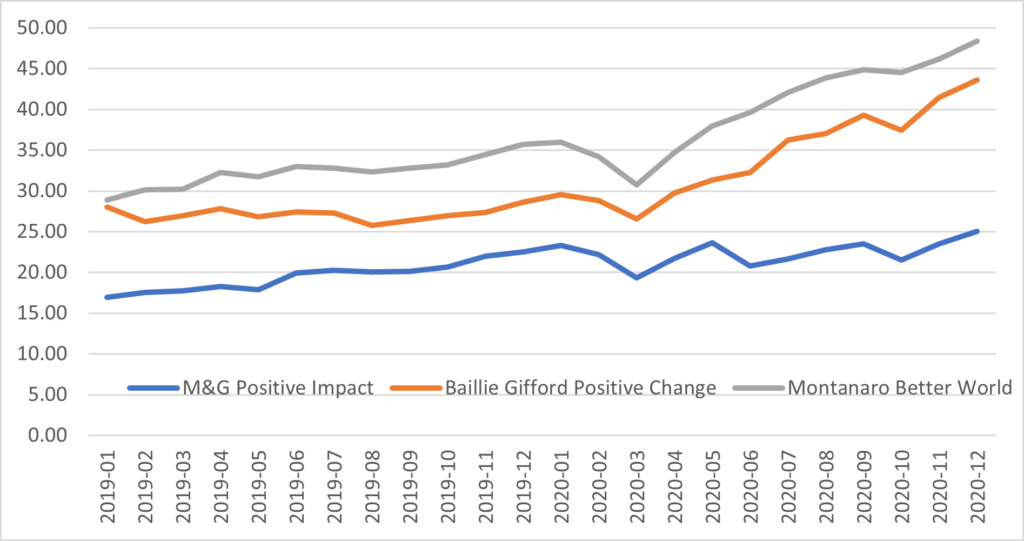

Turning to what’s worked in terms of performance in markets across the past year to 18 months, it’s clear technology and themes linked to ESG have outperformed. This has helped these three funds outperform their respective indices over this period. But it is useful to cast an eye over what that means on a valuation basis for the portfolios as a whole.

Portfolio P/E for each month over two years

M&G Positive Impact has hovered around the 20x PE mark over the past year, whereas there has been a clear spike upwards from the Montanaro and Baillie Gifford funds, which are also displaying high momentum.

The main reasons for this are that Montanaro Better World has nearly double the exposure to technology compared with the other two, while Baillie Gifford’s consumer cyclical exposure stems from Tesla, Mercado Libre and Alibaba. Tesla has been owned since the fund’s launch in March 2017 and has grown from a 6.9% position at that point to 9% at the end of December 2020. Its meteoric rise over the past year has meant that at times, the portfolio managers will have been forced to actively trim the position in order to keep the size in check.

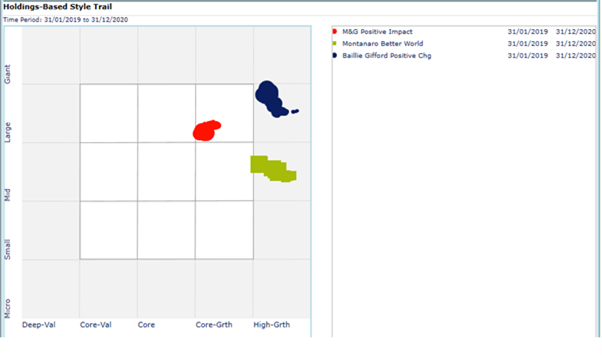

Finally, the Morningstar Style Box shows market cap exposure on the vertical axis and value versus from growth, from left to right respectively over two years to end December 2020.

Impact funds generally have a leaning to growth, with Montanaro Better World and Baillie Gifford Positive Change sitting on the high growth side. This is in keeping with the style we tend to see from most of these groups’ other offerings.

But when discussing impact funds with clients and thinking about how they fit in a wider portfolio, it’s important to think about biases in sectors and style, plus involvement in certain activities and how that all fits into the aim of doing good and measuring impact.