Investor pressure on asset managers to categorise their funds as Article 8 or 9 under the Sustainable Finance Disclosure Regulation (SFDR) has led to a broad and varying range of funds being listed under Article 8 that could cause further misunderstanding and greenwashing.

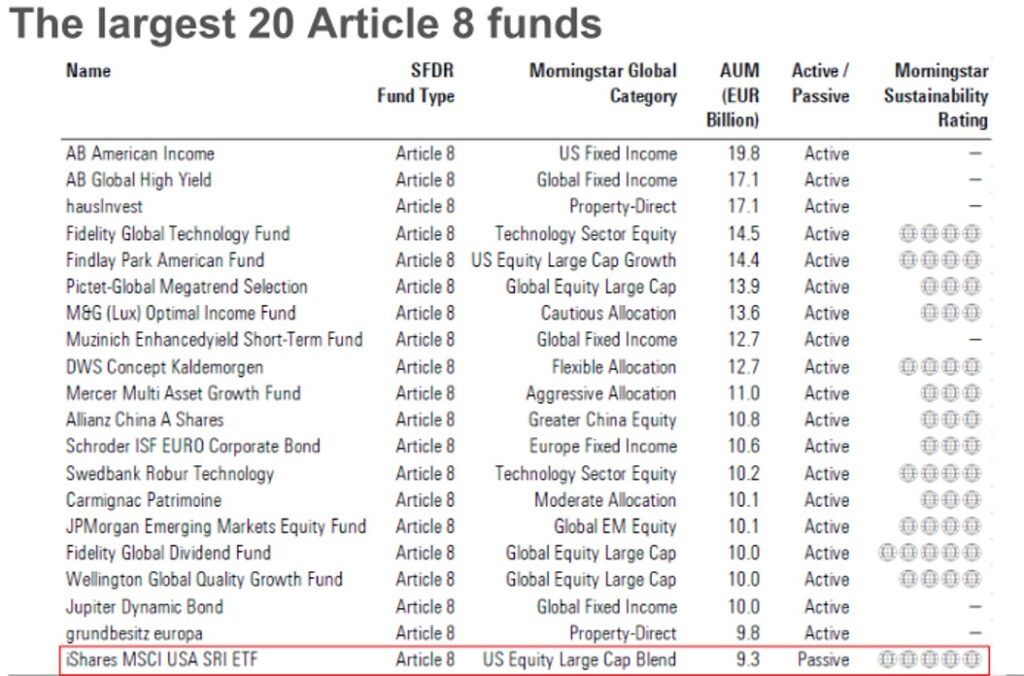

One year on from when SFDR was introduced, Morningstar research has found that out of the top 20 largest Article 8 funds, only one has a reference to responsible investing in its name – the iShares MSCI USA SRI ETF.

Hortense Bioy (pictured), director of global sustainability research at Morningstar and member of the ESG Clarity Committee, commented: “There are many funds as classified as Article 8 that do not look ESG – this may come as a surprise to investors.

“The fact is, these funds are required to consider ESG but do not have ESG-binding criteria.

“This is where there has been confusion in the market, and it is giving asset managers the chance to greenwash; they are saying the fund is now categorised as Article 8 but nothing in the investment objective or portfolio has changed.”

Demand

Looking at data from December 2021, Article 8/9 funds represented more than 42% of Europe’s fund assets, with a combined assets under management of €4trn. Some 25.2% of this segment is Article 8 while just 3.4% is Article 9.

Over the past few months, Morningstar has seen increased flows into Article 8/9 funds, while Article 6 funds – the “stealth” category for other remaining funds – has seen a decline.

Morningstar expects AUM and flows into Article 8/9 funds to increase as asset managers enhance and/or reclassify existing strategies and launch new funds – it estimated that Article 8/9 fund assets could reach half of total assets in scope of SFDR by mid-2022. This will also be spurred by retail flows into sustainable funds as financial advisers will be required to ask clients about their sustainability preferences under Mifid II from August.

However, investors are being urged to carry out their own research on funds particularly within Article 8.

“SFDR has been helpful in dividing up a huge universe, but investors really need to carry out their due diligence on the different shades of green within Article 8/9 funds to understand the nuances between ESG approaches,” said Bioy.

“Asset managers have taken different approaches to classification and we can see similar strategies in both categories.”

She pointed out Article 8 has a bit of a “catch-all” approach with asset managers including funds in this category if they mention ESG – they tend to have an exclusionary approach and even a lower carbon intensity than benchmark, but do not have any binding constraints – they simply say they will consider ESG factors.

However, it is a different story for Article 9 funds: out of the top 20 largest strategies, 17 have a sustainable reference in their name. The three that do not, Bioy said, have a clear ESG strategy as the two Handelsbanken funds have switched benchmarks while the Carmignac fund recently adopted an alignment with the UN Sustainable Development Goals (SDGs).

“Article 9 funds, the dark green category, see many funds with an impact focus or there are thematic funds that have a positive screening.

“But we are also seeing strategies that are similar to what is included in Article 8. This suggests some managers have been conservative and others too generous.

“However, asset managers with more Article 9 are clearly more confident in their ability to demonstrate their sustainable investment and objective.”

She also highlighted that the asset managers with the most Article 8/9 funds since SFDR was introduced on 10 March last year has stayed the same with Amundi, Nordea, Swedbank, J.P. Morgan and BlackRock at the top five. However, their market share has reduced as more groups classify funds.

“Groups are under pressure from buyers who have said they will only consider Article 8/9 funds going forward.”

BNP Paribas see highest market share increase from 16th to 6th place.

See also: – EU delays phase two of SFDR implementation

Fossil fuel exposure

Another surprising element from the research was that fossil fuel exposure in Article 8/9 funds had actually increased. Bioy explained thermal coal involvement had declined with more Article 8/9 funds having either zero or lower exposure, due to “the more systematic exclusions of the worst carbon-intensive companies by asset managers”, but on the flip side, Article 8/9 funds involvement in fossil fuels across the board has increased over the past six months.

“This is perhaps not surprising, given the rally in oil and gas prices last year, which have mechanically increased the revenue of oil and gas companies and the share price, and as a result, portfolio exposure to these companies.

“The high fossil fuel involvement of Article 9 funds in particular may come as a surprise to investors. This is because they have chosen to invest in transitioning companies (oil and gas/utilities companies that have made a commitment to move away from carbon intensive activities and have set net zero emissions targets. These also include oil and gas/ utilities companies that are increasing their exposure to renewable energy but are still operating their legacy fossil fuel businesses).

Future refinements

With the varying strategies being classified, the differing approaches taken by asset managers, and increasing concerns around the opportunities to greenwash, it is expected that there will be adjustments to SFDR requirements in the coming years particularly as separate countries are looking to adopt their own frameworks around disclosures and labelling.

See also: – Q&A: How can SFDR be improved?

Andy Petit, director of policy research at Morningstar, said Spain, Ireland, Germany and the UK are all looking at developing their own ways of making the different kinds of sustainable funds clearer for investors.

Furthermore, he predicted it is likely regulators will look at introducing minimum sustainable criteria for funds to sit within Article 8, or create an Article 8+ category. There are also a number of other legislations coming up that will have an impact: Ecolabels, the EU taxonomy, and the level 2 Regulatory Technical Standards.

“[The latter] is due to be in place later this year and will include fixed form disclosure templates, [which Article 8 and 9 products will have to publish both on a pre-contractual basis and then on an ongoing periodic reporting basis]. We will see far more detailed data in terms of the characteristics being promoted and in terms of metrics to support and show how those objectives/ characteristics are being pursued and with what level of success. This should provide more transparency for investors,” Petit said.

He added the taxonomy alignment is a challenge due to the “data and timeline mismatches” – corporate disclosures about how much revenues/capex are aligned to taxonomy activities have been delayed until 2023 for non-financial companies and 2024 for financial firms.

“This makes things very difficult for product providers – the rules for governing products are running significantly ahead of corporates.

“With that disconnect, my colleagues are finding they have to say in the absence of that data they are unable to set targets without that underlying measures in place. It will be interesting to see how it pans out for the rest of the year.”

However, he added the “regulatory path is becoming much clearer”.