With impact and sustainable mandates rising in prominence, a strong majority of asset owners are currently prioritising environmental (77%) and social (75%) outcomes in their private markets portfolios, a trend set to accelerate over the next two years, according to the latest report published by Legal & General (L&G).

The study of 150 institutional investors focused on key allocation drivers and the increasing importance of impact and sustainability mandates in planning future private market portfolios, showing a clear alignment between commercial returns and the societal and environmental outcomes investors are prioritising.

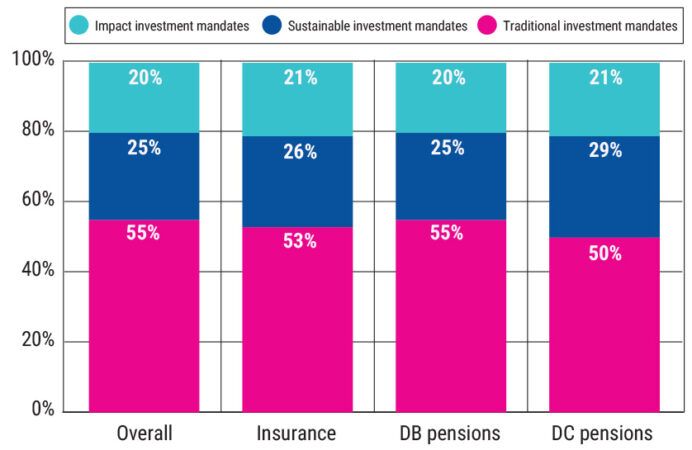

Of the client segments surveyed, Defined Contribution (DC) pension schemes are expected to have the greatest number of impact and sustainable mandates, representing a total of 50% of private portfolios in two years. This is closely followed by insurance investors at 47% and Defined Benefit (DB) pension schemes at 45%.

Bill Hughes, global head of private markets at L&G, said: “As we set out earlier this year, our ambition is to expand our global private markets platform, giving clients access to a breadth of investment opportunities, particularly in private credit, real estate, infrastructure and venture capital. This research confirms that investors are looking to increase their allocations to private markets for the potential increased returns they can deliver, in addition to their sustainability and impact characteristics.”

Environmental and social priorities

Over three-quarters (81%) of investors said that clean energy and tech, and renewable energy infrastructure, were the top environmental outcomes they were prioritising, identifying these sectors as providing the biggest investment opportunities in the near future. This was followed by sustainable transport (46%) and sustainable real estate (36%).

Economic infrastructure (52%), health and social care (43%) and affordable housing (41%) are the social outcomes that are highest on investors’ agendas within private markets. Additionally, over half (57%) of DC investors said life sciences was a top priority among social issues, alongside healthcare outcomes (53%). In contrast, economic infrastructure (49%) and affordable housing (41%) are the top social outcomes for Corporate DB schemes.

Expected breakdown in two years’ time

Meanwhile, when surveyed on the most attractive thematic trends to target via private markets, almost three-fifths (59%) of respondents said the climate transition and decarbonisation.

As a result, institutional investors seek to increase their allocations to the following sectors in order of priority: infrastructure, private equity/venture capital, private credit and real estate. 53% of those surveyed plan to increase allocations to infrastructure over the next two years, with 43% set to also increase private equity and private credit.

DC schemes are prioritising transmission assets and network resilience to a greater extent than other investors, with 47% citing this as a priority area. In contrast, LGPS are the most likely cohort to see nature-based solutions as offering the best return opportunities (20% compared to DC at 17% and insurers at 11%).

Christy Lindsay, head of private markets distribution, L&G Investment Management, added: “This research allows us to gain a comprehensive overview of the opportunities and challenges institutional investors face in allocating within private markets. In our view, this can only grow in importance as a result of changing market and regulatory dynamics. As a long-standing investor in many of these critical sectors, we are well placed to help clients navigate their future private markets allocations.”