As the global population grows, the negative environmental impacts of our demand for fashion are becoming more apparent. The industry is responsible for 10% of global carbon emissions and 20% of global wastewater, as well as producing significant amounts of waste. The equivalent of one garbage truck of textiles is dumped in landfill or burned every second.

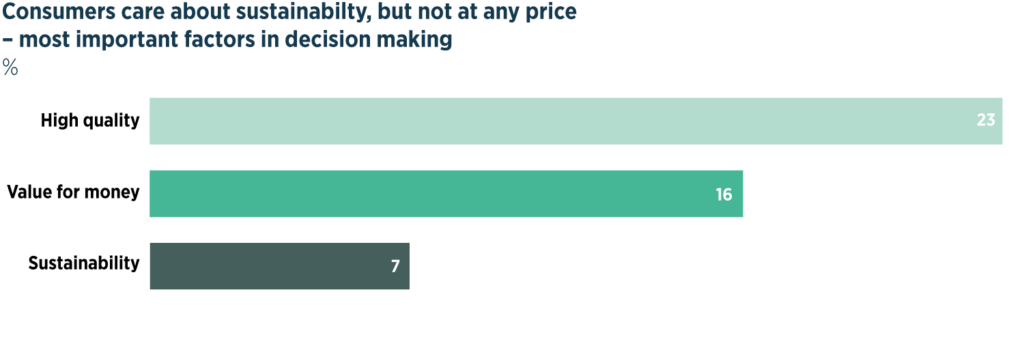

75% of consumers view sustainability as ‘extremely’ or ‘very important’ in their fashion purchasing decision. And over 50% of consumers would switch for a brand that acts in a more environmentally and socially friendly way. But in practice, are consumers really willing to pay? Not yet, it seems. Only 7% of consumers say sustainability is the most important factor in their decision making.

Consumers continue to rate ‘high quality’ and ‘good value for money’ as the most important factors in their decisions. This is backed up by our engagements with fashion companies, who claim that consumers are not willing to pay a premium for sustainability, although at the same price point they would choose the more sustainable offering.

To us, this signals that consumers have a preference for sustainability and it can be a competitive advantage for retailers. But companies need to see it as a way to maintain or grow their market share rather than a way to increase prices. Sustainable leaders should be investing in innovation and scale for sustainable solutions to bring prices down and maintain their brand position.

Distinguishing the real from the fake

The fashion industry is highly fragmented, and sustainability standards are still in their infancy. More and more companies are reporting on both their environmental and social impacts. But with different companies focusing on different disclosures, metrics and measurement methodologies, how can we identify the best? Fundamental research and company engagement are key, allowing investors to assess whether fashion brands are paying lip service to sustainability or whether they are truly committed to it.

There are three things we look for when identifying a sustainable fashion leader. First, has the company signed up to measurable targets to reduce its negative environmental footprint? Second, is the company abiding by external certifications to demonstrate the sustainability of its products? And third, is the company accurately measuring and reporting its entire carbon footprint?

The last of these requires particular research focus as only about 5% of a fashion retailer’s carbon footprint comes directly from its own operations (scope 1 emissions) or indirectly from generating the energy used by the company (scope 2). The vast majority of carbon emissions occur in the company’s value chain (scope 3). This includes production, processing and transportation of fibres and fabrics, transportation of the end product to its final destination, and emissions related to use, care and disposal. Unsurprisingly, this complexity means that emissions are currently underreported, with many companies only reporting on transportation of the end product. Fundamental research is therefore key to understand the supply chain picture and determine what companies are really doing to reduce their total emissions.

Adidas is a good example of a company at the forefront of sustainability within the fashion industry. The well-known sportswear brand particularly stands out on circularity, which is embedded in its strategic priorities. By 2024, Adidas has committed to replace virgin polyester with recycled polyester. The company already partners with the environmental organisation Parley for the Oceans to use recycled polyester made out of plastic collected from the coastline. All of Adidas’s cotton is sustainably sourced via the Better Cotton Initiative, earning Adidas the top spot in a 2020 independent ranking on sustainable cotton sourcing. Adidas has also committed to reducing greenhouse emissions across its entire value chain by 30% between 2017 and 2030, and achieving climate neutrality by 2050.

While price sensitivity remains key for consumers in the fashion industry, evidence points to sustainability becoming more important in purchasing decisions and ultimately to long-term brand value. This implies a material opportunity for sustainable leaders to stand out while unsustainable fashion brands lose out. Yet the potential for greenwashing is rife in the industry, making it difficult to distinguish between leaders and laggards in the transition to sustainable fashion. Company research and engagement is going to remain key.

This piece was co-authored by Joanna Crompton (pictured) and Alexandra Sentuc, portfolio managers on JPMorgan Funds – Europe Sustainable Equity Fund (SICAV) and Bilquis Ahmed, research analyst at J.P. Morgan Asset Management