More and more national regulators are mandating reporting in line with the Taskforce for Climate-related Financial Disclosures, but as this is being adopted to varying degrees in each jurisdiction, investors are encouraged to keep up pressure on corporates to fully disclose voluntarily.

An MSCI report, As TCFD Comes of Age, Regulators Take a Varied Approach, authored by Emma Wu and Zohir Uddin, senior associates for firm’s research department, called TCFD recommendations a “landmark reference for investors trying to integrate climate risks” and found that more than 2,600 organizations – including 1,069 financial institutions with a total of $194trn in AUM, have signed statements in support of the recommendations.

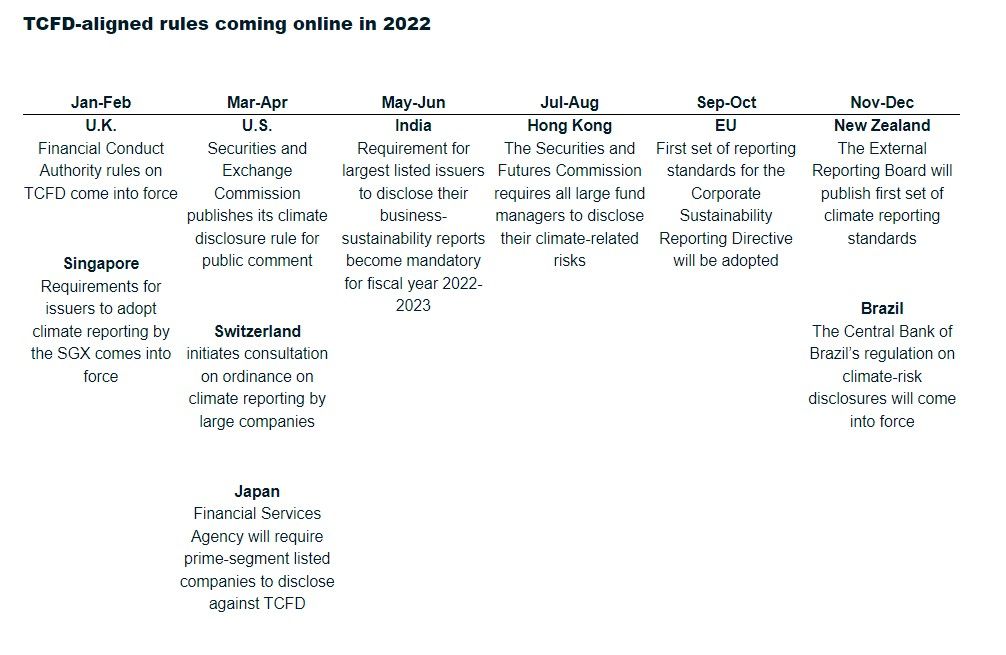

“As these rules come into effect, investors will get access to clearer climate-related information from companies,” the MSCI report said.

Regulators are also stepping up – the UK was the first country to mandate TCFD and many organizations will need to report from 2023, and over the next 12 months at least 10 major economies, including the US, will start to introduce TCFD-aligned disclosure rules for listed companies, large firms and/or financial institutions.

Divergences

However, the MSCI highlighted that regulators are taking different approaches to implementing reporting requirements, calling it a “mixed bag.”

For example, regulators differ in their requirements for forward-looking metrics, transition plans and scenario analysis, with France and New Zealand setting a higher standard than Canada and India, which do not include scenario analysis in their climate disclosure proposals.

Meanwhile, MSCI reported inconsistencies in the scope of firms captured by national climate disclosure rules.

“Whereas the UK, includes all listed firms, financial institutions and large private companies, other jurisdictions such as Brazil and Hong Kong currently plan to require only financial firms to disclose their climate risks,” it said.

Furthermore, there is regional divergence regarding the concept of materiality with the EU adopting a “double-materiality approach,” including both financial and impact materiality, as part of its disclosure requirements, and China following suit.

In the US, however, MSCI explained there is a strict focus on financial materiality, consistent with the recent draft climate-related disclosure requirements from the International Sustainability Standards Board, which are closely tailored to the TCFD framework.

A ‘better problem’

Nonetheless, Linda-Eling Lee (pictured above), global head of ESG and climate research at MSCI, told ESG Clarity the “leap forward” in terms of corporate disclosure is the key takeaway from the research.

“It is important to understand that it is a better problem to have when compared with a few years ago, when we had very little data, it was incomparable, sparse and voluntary based.

“In the world of ESG disclosure, the climate piece has made the most traction as the TCFD has been successful in setting up a comprehensive framework and guidelines and has already prompted more companies to voluntarily disclose giving us more data on climate that is more comprehensive than other ESG topics.

“It’s a good thing from an investor’s perspective that regulators are becoming more focused on this, and that the TCFD framework gives them a common touchpoint to build mandatory disclosures on the same framework.”

Kate Elliott, head of ethical, sustainable and impact research at Rathbone Greenbank Investments, agreed: “In an ideal world, we would have seen global harmonization in TCFD reporting requirements.”

Mikkel Bates, regulatory manager at FE fundinfo and ESG Clarity Committee member, agreed this is a huge positive, but urged fund managers to continue to push companies for more detailed disclosure.

“Much of ESG disclosure is dogged by inconsistencies around the world and TCFD is no different,” he said. “On the face of it, at least investors in each country will be able to compare investments, as the disclosures are consistent within countries, but the different disclosure rules are likely to make it difficult to report fully at a fund level if the underlying companies are not required to disclose the information.”

This is particularly pointed for global investors as the MSCI research forecast this fragmentation will likely continue.

It said: “All indications suggest we will continue to see a rise in TCFD-aligned rules around the world. Wider adoption may be seen as a trend toward greater convergence across markets; but based on a closer examination of how regulators are translating TCFD standards in their respective jurisdictions, our research suggests that national disclosure rules may continue to diverge.”

MSCI’s Lee agreed investors will need to keep the pressure on groups to disclose the gaps left by regulation on a voluntary basis, keeping the momentum going from the past few years.

“What investors should not expect is that [TCFD] is some sort of silver bullet. Over recent years, we have seen investors exercise more active engagement and ownership, and they really can’t let up on that as regulation comes in.

“They need to keep that pressure up to fill in some of the gaps in data on a voluntary basis.”

However, some companies will do this anyway, commented Rathbone’s Elliott: “In reality many companies will report more than the bare minimum they are required to, as they seek to demonstrate to investors and other stakeholders that they are properly managing climate-related risks and opportunities.

“Companies which do not meet expectations on the quality and scope of climate-related disclosures will very quickly find themselves subject to investor scrutiny, with consistency and standardization in global TCFD reporting likely to increase over time.”

Bates reiterated data quality will continue to improve as a result of more regulators mandating TCFD and that is a huge step for the industry. This will be reinforced when the ISSB announce their framework, likely to be implemented as early as next year.

“TCFD recommendations are due to be replaced in many countries by the ISSB standards as the baseline when they are finalized. Not only will those standards go beyond the TCFD’s climate-related disclosures, but if listed companies in all those countries that apply IFRS standards start reporting to the ISSB standards, then the quality of data should be better and more consistent.”