Flows into sustainable funds have cooled significantly in recent years. Regulatory issues and greenwashing concerns have certainly played a role, but it is likely that performance considerations have also contributed to the slowdown. In fact, sustainable funds have broadly underperformed their conventional peers since 2022, which contrasts with their strong performance in previous years. The underperformance also feeds into the common argument against sustainable investing that it potentially sacrifices returns by excluding parts of the market.

Another common assumption is that sustainable investing comes with certain factor tilts that are potentially important drivers of a fund’s relative performance. The most commonly heard are a growth bias and a sector allocation that is heavily skewed toward technology stocks. In a recent study, Morningstar looked at several factor exposures of sustainable equity funds to assess if there were significant differences between conventional and sustainable funds.

The study examined sustainable equity funds in four Morningstar categories (Europe large-cap blend equity, global emerging-markets equity, global large-cap equity blend, and US large-cap blend equity), which are considered core building blocks of the equity part of a portfolio, for their size and style exposures, as well as regional and sector allocations, relative to their conventional peers and category benchmarks.

The study found active sustainable funds have a growth bias relative to their conventional peers and category benchmarks. Although the magnitude of this bias varies across categories, the overall conclusion was that the style bias is limited and probably much smaller than many investors would assume. Meanwhile, sustainable funds tend to shy away slightly from mega-caps, although this also doesn’t translate into an outright overweighting of the smaller-cap portion of the market.

On a sector-relative basis, sustainable funds, unsurprisingly, had little or no allocation to the energy sector on average. The technology sector appeared to be a preferred investment area for sustainable funds. However, the degree of overweighting is quite limited. For example, the median sustainable fund had an overweighting of less than 2% in the sector relative to its conventional peers. Healthcare was also generally overweighted but to a lesser extent than technology.

See also: Next Generation with Morningstar’s Wang: Developing expertise in transition funds

Finally, regional allocations were examined, with a particular focus on the category for global equity funds. The results showed that, on average, active sustainable funds had higher allocations to North America and lower allocations to Asia and emerging markets. However, the magnitude of the differences in regional allocations was limited.

The overall conclusion of the study is that sustainable funds do exhibit factor tilts, including some that are widely assumed by investors. However, the magnitude of these biases is limited and probably much smaller than often assumed. To illustrate that investors can move their conventional funds into sustainable funds without adding factor risk, we present three sustainable funds in which Morningstar’s manager research analysts have expressed positive conviction, but without undue factor risks.

ABN AMRO Funds – Parnassus US ESG Equities

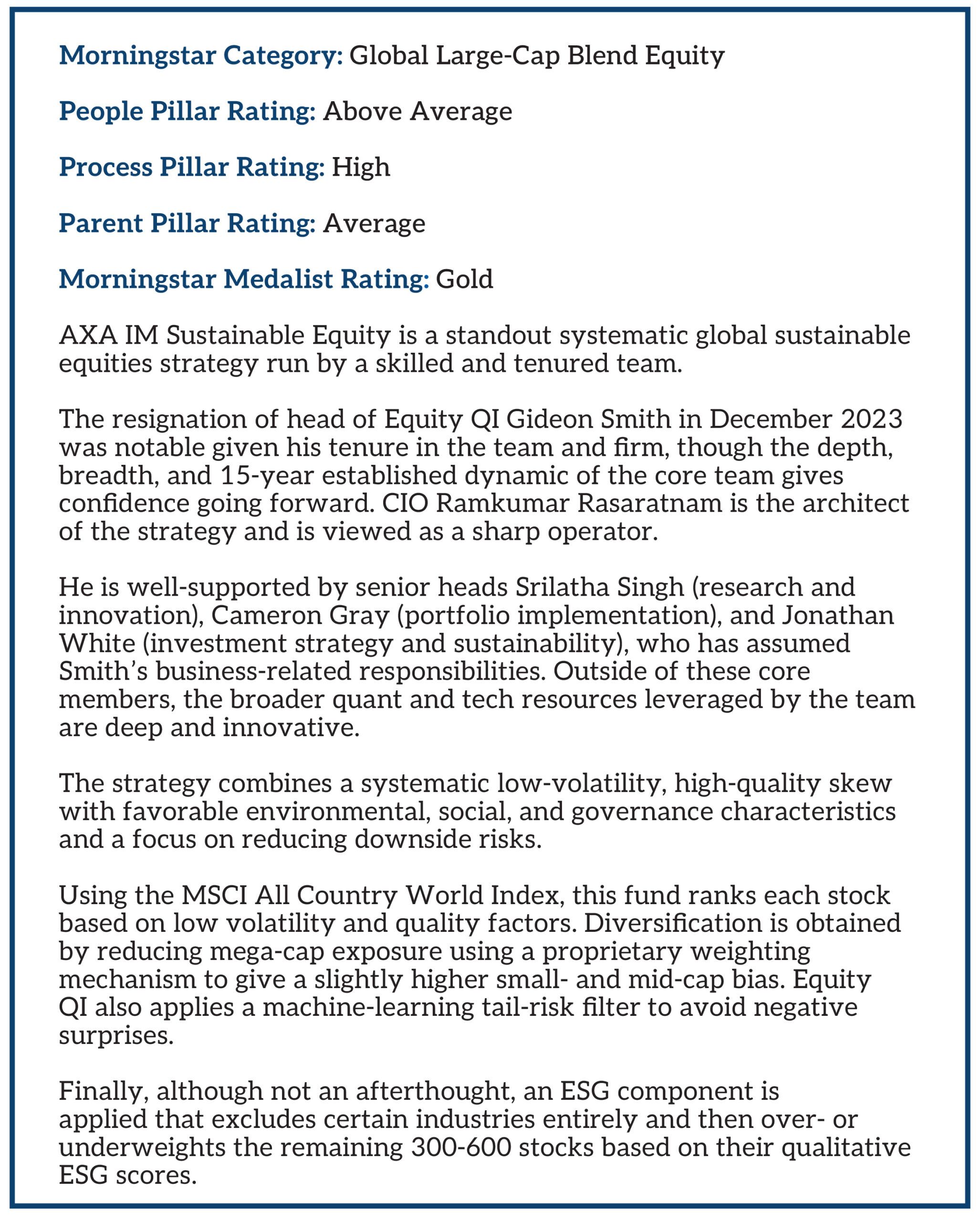

AXA World Funds – Sustainable Equity QI

M&G (Lux) Pan European Sustainable Paris Aligned fund