Climate change is no longer an issue for future generations, nor an issue the asset management industry can continue to overlook. Its impacts are increasing in scale and severity.

Last year alone saw some of the highest temperatures ever recorded, while increasing areas of the globe are simultaneously struggling with drought and heavy rainfall. Without a significant decrease in global emissions, the physical impacts currently being experienced will only escalate.

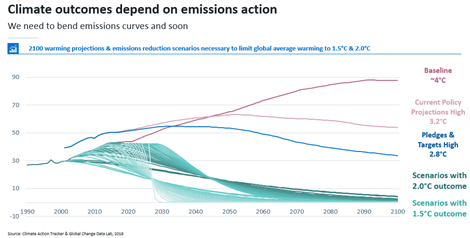

The Paris Agreement represents a commitment to limit the increase in global average temperature to well below 2°C, and aiming for 1.5°C. At current emission rates, global temperature trajectories will clearly exceed these Paris targets.

Accordingly, to deliver on the Paris Agreement aim of making finance flows consistent with a pathway towards low emissions and climate-resilient development, we must both increase climate investment significantly and shift capital away from fossil fuels and other emissions intensive activities.

What does this mean for the investment industry?

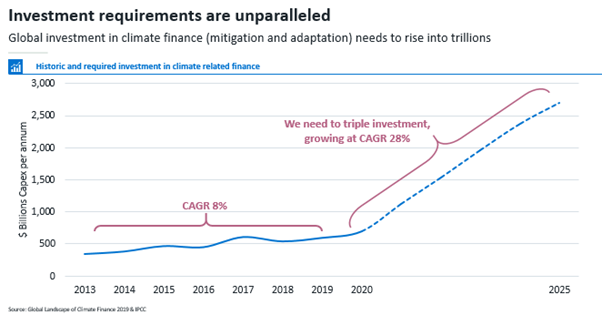

Using data from the Global Landscape of Climate Finance 2019 and the Intergovernmental Panel on Climate Change, we estimate that to achieve net zero, the global economy will need to triple climate-related capital expenditure to in excess of $2.5trn a year by 2025. This equates to a compound annual growth rate of some 28% over the next five years. This is not a one-off cost, but an ongoing allocation of capital, directed towards a range of opportunities: renewable energy, smart grids, agriculture and battery storage, to name just a few.

As a thematic investor, we look for the long-term trends that are shaping our world for decades to come. As climate change rises up the agenda, regulations tighten and capital flows shift, those companies that will benefit from the shift represent a significant investment opportunity. This is why climate change is one of our five core themes.

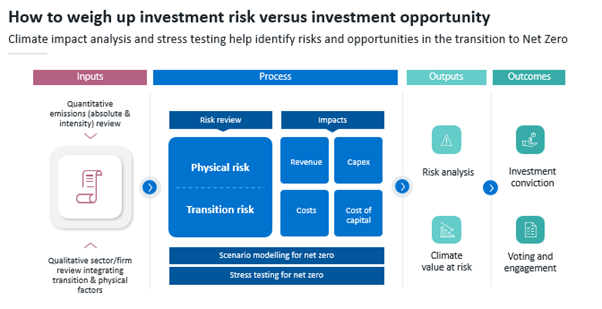

Weigh up risk and opportunity

When looking at a company’s ability to deliver long-term performance, we seek to identify those that are well-positioned as the global economy transitions to net zero. These opportunities can be categorised as those mitigating the impacts of climate change and those focused on delivering adaptation solutions for society and the economy.

However, we also need to understand which companies and sectors are most likely to suffer from climate-related risks. To do this, we analyse the implications of company-specific net-zero pathways, as well as the risks stemming from the increased physical manifestation of climate change.

In assessing the risks and opportunities to come, we consider a range of quantitative factors, such as a firm’s emissions, and qualitative factors, such as the ease with which sector, or firm specific emissions may be abated.

We then apply this understanding of transition and physical risks to our financial forecasts, building a picture of how climate change scenarios could impact revenues, costs, capital expenditure and cost of capital.

Ultimately, this process enables us to calculate a firm’s climate value at risk (CVAR). This metric is one we have developed to illustrate the economic value at risk from climate change. A numerical measure of risk allows us to easily measure how the climate risk of a portfolio changes over time, as well as compare specific companies and industries.

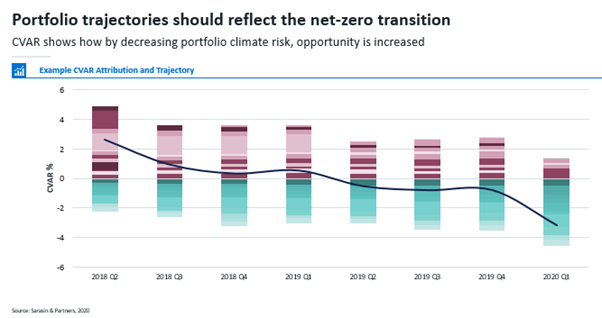

Applying these bottom-up company CVARs allows us to generate aggregated portfolio level CVAR, positioning funds to benefit from reduced climate risk and increasing the exposure to companies positioned to deliver mitigation and adaptation solutions.

With contributions from Ben McEwen, climate change analyst, Sarasin & Partners.