As the world continues to grapple with climate change and energy security, solar energy is emerging as a pivotal long-term solution. This is particularly true in the technologically advanced US, which boasts abundant sunlight and a large landmass. However, while the fundamentals are sound, understanding the drivers of solar electricity pricing is crucial to identifying areas for investment returns.

Across the US, state-level mandates for renewable energy have and continue to be key for increasing the proportion of electricity generated from renewable sources. These policies are crucial in shaping the landscape of solar power pricing.

For instance, California, the leader in solar installed capacity, has continually increased its Renewable Portfolio Standard (RPS) – a regulation mandating increased generation of electricity from renewable sources. North Carolina, despite having less favourable solar resources than most southern US states, is the number four state by installed solar capacity and has had its own RPS since 2007. Although Florida lacks a statewide RPS, or a voluntary renewable energy target, cities within the state and resident utility companies have decarbonisation targets to drive renewable procurement, placing Florida third in terms of installed solar capacity.

These objectives at state and local levels drive demand for electricity generated from renewable sources. Therefore, as a result of state-level objectives, the overall demand for electricity generated from all sources – including hydrocarbons – is not necessarily linked to the demand for renewable energy. In many cases, due to these mandates, buyers will continue to demand renewable energy even when supply decreases and costs increase.

Supply-demand imbalance

In contrast to historical trends and long-term projections for the sector, recent trends have seen increases in Power Purchase Agreement (PPA) prices – a contractual agreement between a power generator and buyer. Notably, PPA prices increased by 15% year on year to December 2023 – due to increased financing costs from higher interest rates, supply chain issues, and increasing demand for renewable PPAs.

Over the medium term, forecasters in US energy markets predict stable or declining prices through to 2030, with modest increases thereafter due to increasing demand from EVs. Declining prices are usually attributed to supply chain stabilisation, federal tax credits under the Inflation Reduction Act (IRA), and an ever-reducing cost of components such as solar panels.

Despite this potential for declining prices, the current imbalance between new renewable project supply and renewable electricity demand leaves the possibility of sustained increases in the price of renewable PPAs as very realistic in the medium term.

Lagging development

In 2023, the US installed a record 31 gigawatts (GW) of solar energy capacity, marking a 55% increase from 2022 and surpassing the previous record set in 2021.

However, to become 100% carbon-free electricity by 2035 – essential for achieving net-zero greenhouse gas emissions by 2050 – annual renewable energy installations must nearly double the levels seen in 2024. At current rates of construction, demand for renewable energy will be significantly unfulfilled by the supply. In this scenario, in the absence of RPS or CES (Clean Energy Standards), prices would be expected to rise rather than stabilise or fall.

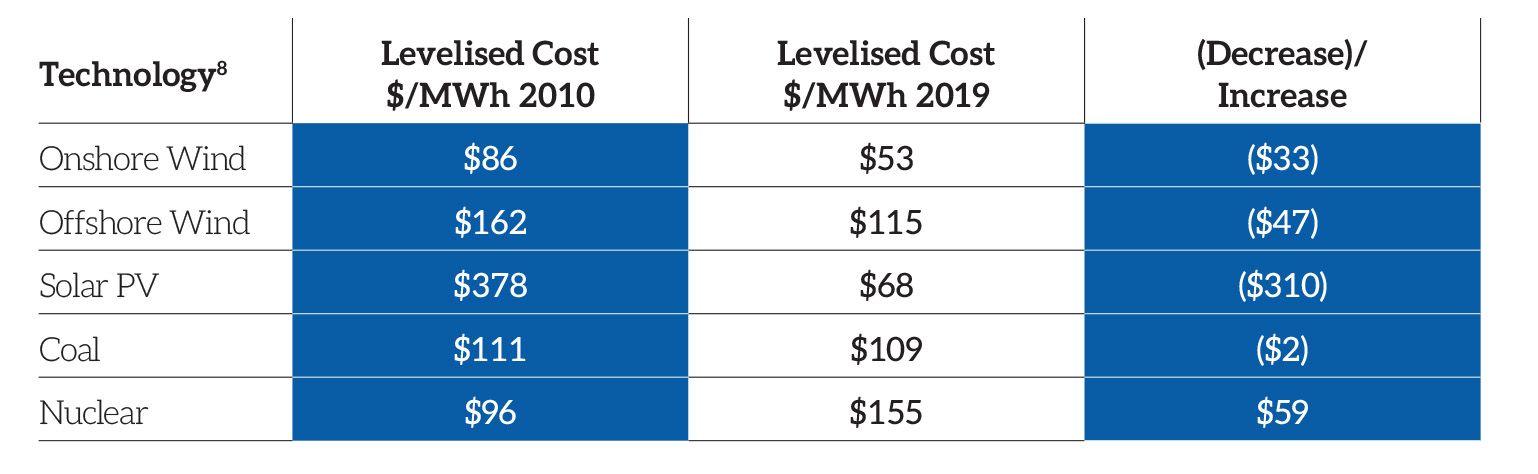

Typically, the counterargument suggests continued reduction in the cost, and improvements in the generation capacity of panels, coupled with federal incentives, will result in very cheap power being available at a very large scale to satisfy the demand. However, this has not been the case for other technologies – such as nuclear, coal and gas. This discrepancy highlights a unique challenge for solar energy, which is already becoming apparent in both the US and European markets.

Cost complications

Efficiency gains, or ‘learning rate’, associated with solar and other renewables have historically been impressive. However, even as the production costs of solar components reduce, other factors like construction pricing, costs of connecting to overstressed grid networks, and legal challenges to permitting obstructions are increasingly impacting the overall costs of new projects.

While reductions in module pricing, supported by federal and state initiatives such as the Inflation Reduction and CHIPS and Science Act, may offset some of these non-module-related cost increases, it is uncertain if domestic module pricing can undercut non-US panels. In the past two years, these non-module-related costs have notably driven up the prices that buyers need to pay.

Over the longer term, this trend could continue as the development industry contends with issues such as interconnection delays, permitting reforms, and transmission constraints – which are driving up costs for new projects. This is likely to increase the price that developers demand and the price at which existing operational assets can sell power to the grid.

State and corporate renewable agendas appear to continue to increase based on their current trajectory. However, if the supply of new projects is not capable of generating sufficient electricity to meet this demand, due to issues such as grid-related bottlenecks and high component prices, the overall impact could be sustained increases in PPA prices.