Alternative investment trusts are falling short in terms of corporate governance and responsible investment disclosure, an analytical study carried out by Quilter Cheviot has found.

In particular, the trusts fell down on lack of independence, poor oversight, lack of diversity and communication with shareholders, the research revealed.

Quilter Cheviot carried out engagement with 27 alternative investment trusts within the infrastructure and private equity sectors, as well as other asset classes, by meeting with the chairs and other non-executive directors (NEDs) to discuss the following:

- Board composition – boards should be independent, diverse and have the right skillset.

- Board effectiveness – boards should have the ability and willingness to challenge the investment adviser when necessary and be accessible to meet with shareholders and open to considering their feedback.

- Disclosures – responsible investment disclosures that are pertinent to the investment trust and provide real-life examples of how the trust approaches stewardship and the integration of environmental, social and governance factors within its investment process.

Each trust was ranked red, amber or green rating on the three criteria – only four investment trusts qualified for a green rating in each of the categories, while just one received a red rating across the board.

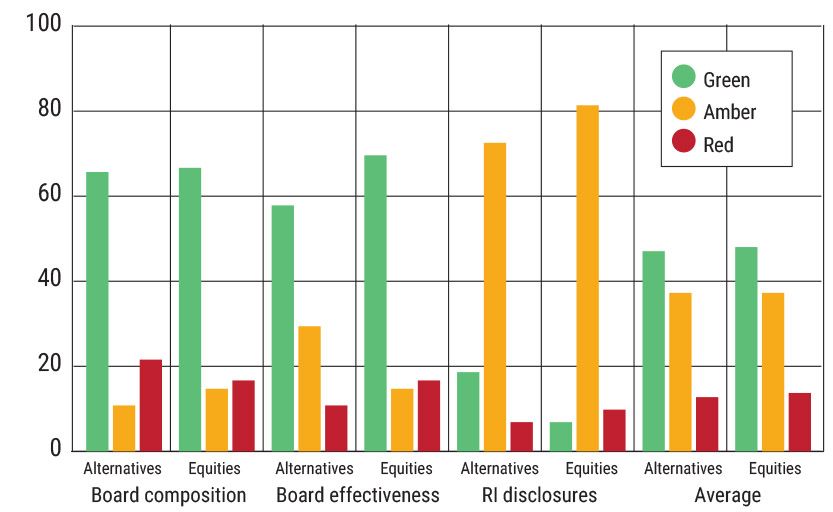

Alternative trusts vs equities trusts

Looking at board composition, some 67% of the alternative trusts achieved a green rating. However, this was also the category with largest proportion of red ratings, with nearly a quarter (22%) receiving a red, as Quilter Cheviot flagged a lack of independence, manager representatives, poor oversight and lack of diversity.

Meanwhile, fewer than 60% of trusts received a green rating for board effectiveness. However, while some boards demonstrated poor communication with shareholders, there were few reds in this category.

Finally, when responsible investment disclosures were analysed some 19% scored a green rating, with just 7% being given a red. However, 74% of the boards were provided an amber rating as a result of a disconnect between responsible investment processes and the disclosure of such activities, Quilter Cheviot said in a statement, as it noted the “direction of travel in this space is good”.

Gemma Woodward (pictured), head of responsible investment at Quilter Cheviot and member of the PA Future Committee, commented: “There is room for improvement when it comes to the corporate governance practices of alternative investment trusts. While alternatives span everything from infrastructure to private equity and multi-asset to music royalties, there is common best practice they can all align to that will benefit shareholders in the long term.

“Clearly investor expectations change over time and what was previously good practice is no longer the case. Indeed, with the likes of responsible investment the pace of change is fast and some can be left behind. This is where activities such as this engagement are meant to be collaborative and ensure boards aren’t falling down when changes can be easily made. We have already seen some really positive improvements from some boards, and we look forward to working closely with the 27 we have engaged with here to help them improve where possible.”

‘Vital boards add value’

PA Future approached the Association of Investment Companies for comment and CEO Richard Stone said: “Quilter Cheviot is a leading investor in investment trusts and it’s good to see their commitment to this ongoing engagement programme. Independent boards are a key benefit of the investment trust structure, and shareholder engagement is vital to help boards add the most possible value.”

Bhavini ‘Bev’ Shah, co-chief executive at think tank City Hive, which is driving transparency and improvements in corporate culture in the investment industry with its ACT framework, commented: “We welcome Quilter Cheviot’s shift in focus. As a standardised framework that captures the corporate culture of investment management companies, ACT can be used by boards of investment trusts regardless of asset class to assess the corporate culture of their current investment advisers who are managing their assets.

“The producer not just the product should be considered as part of governance in order to mitigate risk and understand the environment in which assets are being managed.”